Attending university is a dream for many Canadian students. Undergraduate students have their first taste of freedom from home. Graduate program candidates are enhancing their resumes with advanced credentials. Whether government loans or a private student line of credit, proper financing for your education is vital to keeping your focus on your degree.

Some students will benefit from their parent's early financial planning through a Registered Education Savings Plan (RESP). Other candidates will maintain part-time or full-time jobs to fund their educational ambitions. In any case, a bank line of credit provides a use-and-reuse flexibility that can come in handy while you attend your program of study.

This article discusses the various choices for private student loans and lines of credit and the associated interest rates and monthly payments. You may find that the idea that government student loans are the best option may not be accurate, especially if you live in a province with higher interest rates than a private bank can provide.

Government Student Loans

The federal government permanently eliminated interest on the federal portion of student aid. Students are now only required to pay their respective provincial interest on the provincial portion of the loan.

Creditpicks

Canadian provinces offer different student loan options with different terms and considerations. The National Student Loan Service Centre, hosted by the federal government, also provides a loan plan. This website provides valuable resources, such as an overview of loan info, payments, remaining balance, and projected loan repayment date.

Generally, the process for applying for federal aid is the same as for provincial aid. For example, federal aid and the Ontario Student Assistance Program (OSAP) are applied for simultaneously in Ontario. Nevertheless, if your provincial loan is sufficient for your tuition and living costs, you may decide to forgo the federal loan, mainly if the interest rate is too high.

The interest rate for a federal student loan was previously 0.5% + Prime (with the average bank prime rate changing frequently. However, recently the federal government permanently eliminated interest on the federal portion of student aid. Students are now only required to pay their respective provincial interest on the provincial part of the loan.

We recently wrote and posted a complete guide to government student loans.

Credit for Students in Canada

In Canada, private banks provide many alternatives for students to finance their education. These can range from a student loan to a line of credit to a student credit card, each with its own interest rate.

When you first meet a financial advisor, you will be given different choices depending on your and your parents'/guardians' income and credit score. If your credit score is high, you may be able to get an attractive interest rate.

Student Line of Credit

Most banks provide students with a line of credit, allowing them to borrow up to a certain amount. This money can be transferred directly to their chequing account, so they only have to take out what they need instead of receiving a lump sum. This means that the interest paid is only on the amount used.

For example, if the credit limit is $10,000.00 and only $3,000.00 is used, the interest is only applied to the $3,000.00. So here's the good news: As you pay off the $3,000.00 you used, you can reaccess the amount you have paid off.

So, if you pay off $2,000.00 of the $3,000.00 you borrowed, you can immediately access that $2,000.00 again. This arrangement is called a revolving line of credit.

Banks May Offer Lower Interest Rates

Banks typically offer a lower interest rate for student lines of credit than the government's loan program. This interest immediately starts accruing on any amount accessed. Government loans provide a grace period of six months and payment options. But if you're required to pay interest immediately, this may push you to pay off the loan faster.

What do You Need to Get a Student Line of Credit?

Though each bank's requirements will vary slightly, you will likely need each of the following items to apply for a student line of credit:

- Proof of acceptance and enrollment.

- Photo ID issued by the government.

- Personal financial details such as scholarships, bursaries, and other academic financial support. Also, details regarding any anticipated income while you're studying.

- Cosigner details to include:

- Photo ID issued by the government.

- Letter of employment and their last three months of pay stubs.

- Previous year's T4 (though more information may be requested).

It is not uncommon for students to require a cosigner. However, your cosigner will need to be aware that the line of credit will reflect on their credit report, and they are also on the hook if you do not repay any borrowed amount.

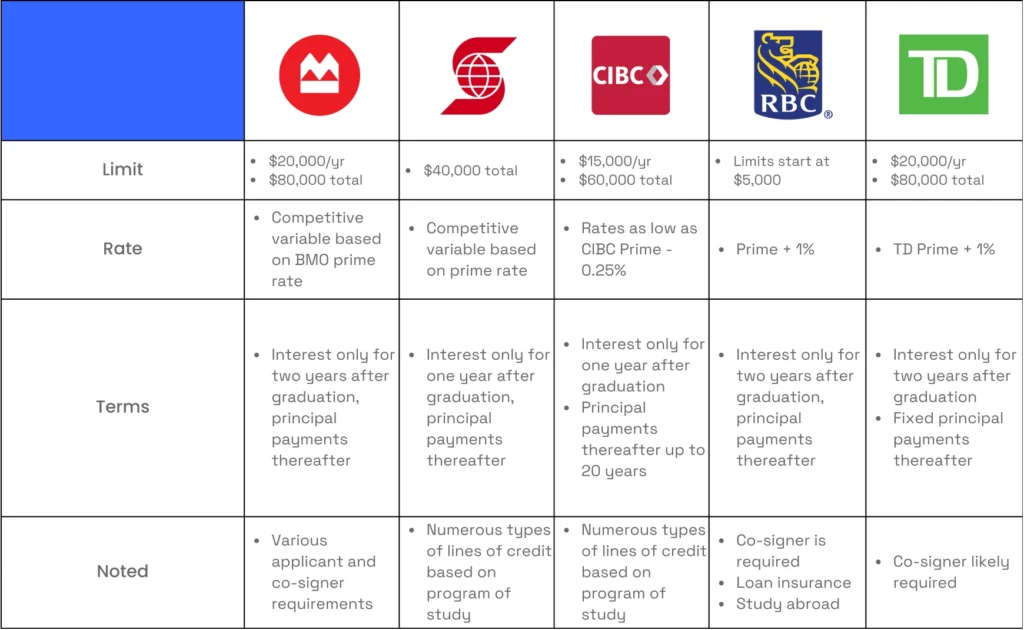

Banks That Offer Student Lines of Credit

Numerous Canadian financial institutions offer lines of credit focusing on student needs. The following table and sections review the Big Five's offerings for students in Canada. Specific program details can change at any time.

Bank of Montreal (BMO)

BMO's Student Line of Credit provides flexible borrowing up to $20,000.00/year, to a maximum of $80,000.00. Like most credit lines, you're only charged interest on what you borrow. Upon graduation, you'll only need to pay interest for two years. Thereafter, you'll begin principal repayments.

Scotiabank

Scotiabank provides a Personal Student Line of Credit with great benefits. Students can delay payments until they've completed their studies, and after graduating, they have 12 months before they have to start repaying the principal. The maximum amount available for full-time students is $40,000, while part-time students can receive up to $20,000.

CIBC

For CIBC's Professional Edge Student Program, you can borrow up to $350,000, depending on your field of study. There is also a standard Education Line of Credit that starts at $5,000 and up.

This line of credit provides up to $60,000 in funds for educational purposes, with an annual limit of $15,000 for full-time students and $7,500 for part-time students. Your loan payments can be spread out for up to twenty years, with interest payments only required up to 12 months after graduation.

Royal Bank of Canada

RBC offers a Student Line of Credit that allows students to defer payments for up to two years after completing their studies. The credit limits range from $5,000 and higher.

TD Canada Trust

TD Bank offers a student line of credit with a two-year grace period of interest-only payments. Once a student has completed their studies, the payments become fixed.

Undergraduate students can borrow up to a cumulative total of $80,000 over their course of study, with annual borrowing limits of $20,000. Students enrolled in postgraduate or professional studies may be eligible for higher loan amounts.

If you want to learn more about taking out a loan from a student line of credit, contact the bank or lender of your choice and arrange a consultation with a financial expert.

Registered Education Savings Plans (RESP)

An RESP is a savings account designed to help pay for a child's future educational expenses. Interest and payments accumulate over time, so by the time the child is ready to go to college, a sufficient amount of money should be set aside to cover a significant portion of the costs.

The federal and sometimes provincial governments will often add grants to RESPs depending on the subscriber's income. The subscriber will also be given a set limit of yearly contributions that won't be taxed as income.

Government grants include the Canada Education Savings Grant (CESG), Canada Learning Bond (CLB), or any designated provincial education savings program. Payments made to the beneficiary while in school must meet the standards set out by the promoter (the bank) to ensure they aren't taxed or otherwise.

Bank Loans for Students Studying Abroad

Those accepted to study at a qualifying foreign university or other educational institution can access Federal and Provincial student aid to help pay for their schooling. Additionally, many financial institutions can provide financing for overseas studies.

Different lenders have different rules for who is eligible for funding, so it is advisable to contact each lender to find out what programs they have and what information they require.

Shop Around for a Line of Credit

Being aware of your rights when taking out a loan or incurring any form of debt is important. Be sure that you are given all the necessary information regarding the loan, such as interest rates and payment plans, before signing any documents. Do not sign until you have received this information and understand your agreement.

Before applying for loans, it is recommended to look into any scholarships or grants available to you. High schools and colleges have resources available to apply for possible scholarships and grants, which can significantly reduce your debt when you finish school.

Finally, take time to shop around for your student line of credit. The banks all want your business, so you'll likely get a great interest rate and repayment terms based on your or your cosigner's credit score. You'll potentially carry for this debt years after completing your education. Be smart about what you commit to.